在发展中国家中最贫困的13亿人口一直依靠木材和干牛粪为主要烹饪和取暖的燃料。……鉴于证据,通过制定政策的方式,来减少作为燃料的石化能源的使用量,是不明智和不公平的。这样的政策将宣判亿万人类同胞将持续生活在贫困中。

在发展中国家中最贫困的13亿人口一直依靠木材和干牛粪为主要烹饪和取暖的燃料。……鉴于证据,通过制定政策的方式,来减少作为燃料的石化能源的使用量,是不明智和不公平的。这样的政策将宣判亿万人类同胞将持续生活在贫困中。

Antonio Vegas García

Recently, we have been exposed to a barrage of news from China: the rising worries about its economic growth, the recent plunge in the Chinese stockmarkets, the devaluation of the yuan, the announced drops in interest rates, as well as in the cash reserve bank ratios, the Purchasing Managers’ Index (PMI) fell, etc. [1]

Nevertheless, the bad news is not the economic indicators, but the government’s reckless interventions in these days. The government seems risking the initiated path by the Economic Reform towards the development, a movement in the bad direction that could become the next Great Leap Backward in the Chinese economic history.

In order to make it clear, we should build up a general idea about the Chinese economy to be able to put together all the pieces of the Chinese puzzle. The chinese economy is huge and extremely diverse (even we can name it as a dual economy in Lewis terms) but we can state that the Chinese prosperity looks like more a mirage than a reality. Of course that double-digit growth has permitted that China has lifted 600 million people out of poverty during 1981-2004 [2], but at the same time, it has sown the seeds of the future economic problems, the shadow of the Chinese prosperity.

Which are those flaws? Mainly the heavy-handed and commanded economy, through the financing part of the economy, whereby the government extract wealth from the people (mainly controlling the interest rates and the exchange rate of the currency), that is used afterwards to prop up the banks that have chunks of bad loans, thereby allowing them to carry on lending money to the unprofitable SOE (State Owned Enterprises). In short, the government has built a system in order to control every single aspect of the economy, which is generating long-term problems, such as shadow banking (even though the term includes a myriad of different non-conventional institutions).

This financial repression can be illustrated with the example of drug prohibition. When the government attempt to forbid the drugs what it gets is a black market where the people can sell and buy drugs according to human necessities (that are subjective), but the black market is not regulated and it is not safe enough for the users, thereby damaging the health of the participants. The more important (and the more repressive is the prohibition) is the forbidden necessity for humans, the more serious will be the suffering of the population. In the case of China’s financial repression it’s exactly the same: given that chinese people neither can take credit freely nor save their money, a black market pops up to satisfy the necessities, with credit of bad quality, thereby jeopardising the long-term perspective of chinese economy.

Under this outlook, the recent headline-grabbing news about china are not surprising whatsoever, but they are showing that the government is doing whatever it takes in order to shore up the binge. That government disposition is a helpful information, since in China everything is depending on the government. Until when the binge will last? Until the government desire unless it runs out of money, like once Larry White told me very cleverly. After all, it looks like that the government does not want to stop it.

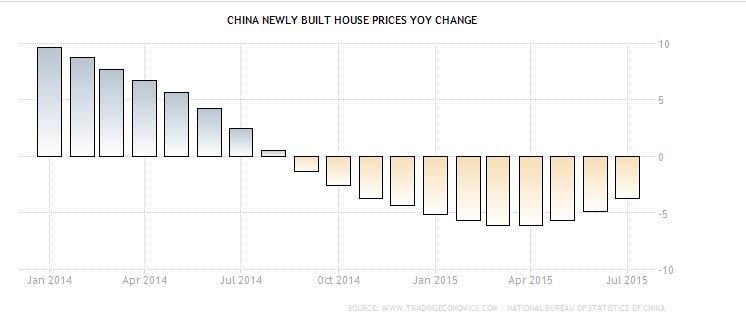

With a slumping housing market, with an entire year of steadily lowering housing prices (see figure 1), the Central Bank of China has been lowering the interest rates one after another (see figure 3), jointly with the cash reserve ratio.(see figure 2), in a last attempt to foster the Chinese economy up to the promised 7% growth rate.

Figure 1: China newly built house prices YoY (Year on Year) change (%) Jan 2014-Jul 2015

Source: Tradingeconomics.com

Figure 2: China cash reserve ratio big banks (%) 2011-2015

Source: Tradingeconomics.com

Figure 3: China interest rate (%) 2012-2015

Source: Tradingeconomics.com

I remember that the summer of 2013 was when I really opened my eyes about the Chinese economy, it was the Shibor (Shanghai Interbank Offered Rate) shock. After an increase of the lending in the first 13 days of June never seen before in history, the interest rates in the interbank market soared to a 12% rate for the seven-day repo [3]. The central bank forced the big banks to lend money to the small banks (with the argument that the overall liquidity within the system was enough), thereby rejecting the inquiry of the financial institutions of injecting more liquidity. One month later, the central bank had to inject a massive amount of liquidity in the system, at the time that the interest rates were lowered as well as the cash reserve ratio. The yield curve (an indicator that it’s used to foresee financial problems in an economy) has not stopped flattening ever since.

The recent plunge in chinese stockmarkets is anecdotal. From the early 2014, the stock indexes reached a high level without any reasonable explanation and mainly driven by credit financing (9% of market capitalization according to Credit Suisse). The price earnings ratio or PER (that is calculated dividing the price of a share over the ratio between the earning of the whole company over the number of shares, namely, the earnings per share, EPS), was in median terms 64 in Shenzhen stock exchange, whereas it is considered that a PER higher than 25 is expensive [4]. The Shenzhen case was paradigmatic. A clear indicator that the Shenzhen Stock Exchange was flying too high.

Therefore, the recent drops in those indexes have been obvious and they have been noticed in advance by Bloomberg or The Economist. And the drops will likely continue for a time. Even though, they are not so troublesome for the Chinese economy in the short-term (because the stock market is not so developed in China as in western countries; its relative size to the economy is small, 40% of the GDP whereas in USA is more than 100% of GDP and the financial culture in chine is still limited) but they will be crucial in the long-run. What is true is that it shows more than ever the shadow of the Chinese prosperity, the financial flaws of the Chinese economy. And the recent actions of the Chinese government are the most burdensome. Let’s see why.

Firstly, in China is urgently needed a complete financial liberalisation, where the bank interest rates can be fixed by the market, with more share of private banks in the economy and the banks being able to give lending according to market criteria and not with political criteria. This will bring the second opening of Chinese economy (the financial opening) and will push the world to a new level of financial globalization. Moreover, it would foster the SOEs to a new level of competitiveness, would give more resources to Chinese private companies and would reduce the power of the government. In other words, it would bring more freedom to Chinese people at a time the shadow of Chinese prosperity shrinks. However, as the recent actions of Chinese government tends to broaden the influence of public sector over stockmarket, the financial liberalisation has fallen to bits.

Chinese stockmarkets were always seen as not so trustworthy but nowadays more so than ever. The government introduced a curb in selling Chinese equities and also it undertook and equities purchasing programme, spending public money in order to prop up the stockmarket bubble. That is added to the enormous requirements that the companies have to fulfil, the daily limitation that a share cannot raise or drop more than a 10%. That is undermining the last bit of truth on Chinese equities.

Secondly, as the equity financing is necessary for Chinese economy in order for the companies to be able to diversify their financing portfolio (debt and equity). Investors were always wary about the Chinese economy and at the time they were surprised that the Chinese economy was resilient to every kind of damage or bad indicators. Investors finally concluded that in China, everything is about its government.

Overall, it looks like that, even though China has advanced until now quite rapidly, a recession would be a necessary step towards China’s development, since the goverment is reluctant to reduce its grip in Chinese economy and it will do whatever it takes to prop up its power, influence and command in Chinese economy. It’s a necessary step that the government runs out of money and the crisis in that sense could be an opportunity. The last government interventions illustrate the government’s disposal to maintain the statu quo, even if that requires to risk the trust of international investors in China or risk positive results of the economic reforms.

Obviously, Chinese economy also has advantages, and it is reducing the importing of inputs to produce the goods that China exports, showing that China is improving in capital accumulation and the economy is more capable to design new products rather than buy them abroad. The attention is in the government’s side. The government still have weapons to shore up the financial mess and its influence on the market, but the money and the time are running out nowadays. What will be the next episode? The crisis in China, will force the government to another set of economic reforms.

–

Notes:

[1] Bloomberg (2015) China’s Official Factory Gauge Shrinks Available:http://www.bloomberg.com/news/videos/2015-09-01/china-s-official-factory-gauge-shrinks [Accessed: 31 August 2015]

[2] CNTV (2014) China has lifted 600 million people out of poverty Available:http://english.cntv.cn/2014/10/18/VIDE1413584528072923.shtml [Accessed: 31 August 2015]

[3] The Economist (2015) Flying too high Available: http://www.economist.com/news/finance-and-economics/21579862-chinas-central-bank-allows-cash-crunch-worsen-shibor-shock [Accessed: 31 August 2015]

[4] The Economist (2013) The Shibor shock Available:http://www.economist.com/news/leaders/21652326-long-term-consequences-chinas-coming-stockmarket-correction-are-ones-fear-flying [Accessed: 31 August 2015]

–

Antonio Vegas García is a researcher from the Shalom Institute and has graduated with a masters degree of finance from the Universidad Carlos III de Madrid (Carlos III University of Madrid).

这个炎热的夏天你开了几天空调?开空调道德吗?

一个国家的真实财富由它的商品和服务构成,而不是黄金的供给。

William Hongsong Wang

On July 15, 2015, Wan Li, a Chinese market reformer in the 1980’s and former Chairman of the Chinese National People’s Congress died at the age of 99, Xinhua News Agency reported.

Like many Eastern countries, China’s market reform was started not by politicians and common people who have a clear theoretical background about free market knowledge but by those who believed that the free market could work better than a centrally-planned system. Wan Li was on of them. After serving in the Chinese Communist Revolution and suffering during the Culture Revolution, top leaders in the Communist Party like Deng Xiaoping, Hu Yaobang, Zhao Ziyang, and Wan gradually acknowledged that the Soviet central planning system was destructive to China. In an effort to escape the disaster and poverty of the Soviet system, these leaders decided to implement market reforms for the country.

After the Cultural Revolution ended in 1976, Wan was nominated in 1977 as the Communist Party of China’s 1st Secretary and Governor of Anhui Province, one of the major agricultural provinces in China. After the devastation of the Cultural Revolution and the centrally-planned system, farmers in Anhui Province were poor, hungry, and inefficient which caused a steep decrease in agricultural productivity. Wan recalled, “In the first year when I arrived in Anhui, only 10% of the production terms had the minimum level of food to eat.” [1]

Before and during the Cultural Revolution, all of the lands, agricultural tools and harvest belonged to the government. Farmers were not allowed to eat the agricultural productions on the farms they were cultivating. Many times as the local government had to do greasiness in Cultural Revolution (If the local bureaucrats wanted to get promotion or praise from their seniors, its’ better for them to report huge political and economic movements to attract attention from their bosses even these plans were totally infeasible), impractical agricultural plans were demanded that made it impossible for farmers to feel incentivized to do their work, provide goods, and earn money. Many farmers died from starvation, and many were executed or punished for not obeying the bureaucrat’s orders by eating the harvest from their own land.

Seeing this as a serious situation, Wan didn’t forbid farmers in Anhui Province from implementing agricultural reform. In the spring of 1978, to resist drought and extreme poverty 18 farmers in Xiaogang Village of Anhui Province began disobeying central plans from senior officials by farming for their own needs and the needs of the local free market in order to make a living. They separated the public farms amongst every individual. All of these individuals were responsible for their own farms and crops and tried their best to grow agricultural products based on their market information. Of course, it was illegal at that time but people there were so hungry that if they didn’t enact the reform themselves, they would not have survived.

This organic spontaneous reform was growing in many villages in the Anhui Province because farmers found that planning their “own” lands could help them earn more money and eat more food which were better than waiting for centrally-planned orders. The economic situation in these rural areas changed rapidly in just a few months after the new free market tests. That year, the farming team of Xiaogang Village’s total grain output was 66.5 thousands kilograms, which was equivalent to the sum of the total food production from 1966 to 1970; total production of oil (mainly groundnut) was 17.5 thousands kilograms, which was equivalent to the sum in whole past 20 years. Due to the development of production, total income of the people in Xiaogang Village was over 47,000 Chinese Yuan, which was 400 Yuan per person and was 18 times higher than the previous year. [2] Famers called this new agriculture institution as “household responsibility system” (包產到戶). This agricultural reform started the famous Chinese “Reform & Opening up" nowadays.

At this time, the reform was becoming a hot political argument in the Communist Party of China (CPC) itself. Some local politicians allowed farmers to do market reform but some did not because they didn’t want to take the risk of losing their jobs or being put in jail for enabling reform without the permission of China’s political leadership. After hesitating for a few months against widespread resistance to deregulation reform among top leaders in the Chinese government, Wan publicly supported the agricultural reforms occurring in the Anhui villages.

Used with the permission of the Central Committee of CPC, other parts of China’s rural areas gradually started doing the household responsibility reform, which allowed every family of farmers to be responsible for their own profit or loss on agricultural production. [3] The result of the reform was so obvious. The year-on –year growth rate of gross agricultural production of China was 8.6% in 1979. The grain production was 33.12 million tons, which was also 8.6% higher than in 1978. The total grain yield increase in 1978 and 1979 was 49 millions tons, which never happened after the establishment of Communist Regime in 1949. [4]

Seeing the obvious result of the agricultural reform, China’s top leaders Hua Guofeng and Deng Xiaoping, who were taking a wait-and-see approach to the situation, finally decided to support the reform in the end of 1979. In 1980, Deng Xiaoping made a speech about that, “After we have introduced more flexible policies in rural areas, the result of the Household Response System was so obvious, which was changing the villages who had adopted the system. … The majority of the production teams in Fengyang County, Anhui Province who adopted the new system has totally changed their economic situation.” [5]

At the same time, it was quickly promoted to other provinces over the next few years and resulted in rapidly expanding agricultural production. In 1982, growth rate of the gross agricultural production was 33.4% higher than in 1978; growth rate of oil crops was 126.5% higher than in 1978; the growth rate of per capita income of Chinese farmers was 102.2% higher than in 1978. [6] In 1982, the market reform in agricultural industry was finally made legal through the approval of Chinese Central Government and was officially named termed the Household Responsibility System.

In 1980, Wan was nominated as one of the vice-premiers of China who continued to support the agricultural reform, market reforms in urban areas and Emancipating of Minds Movement. In 1988, Wan was nominated as the Chairman of National People’s Congress (NPC) to continue to play the role of a reformer in China. However, after the Tian’anmen Square protests of 1989 and the house arrest of Wan’s ally, former General Secretary of CPC Zhao Ziyang, Wan stopped discussing topics related to political freedom such as the liberty of free speech and the democratic reform in China. But instead, as the President of NPC, he devoted more of his time to the legalization of free market activities until his retirement in 1992.

From a libertarian and economic science perspective, comments on politicians should be made unprejudicedly. For promoting liberty, the correct issues Wan Li did for China was to allow spontaneous reform in Chinese rural area even though he was taking a high risk of losing his political future (in the late 1970s and 1980s, market reform was still an unwelcomed and dangerous issue in political agenda and many top CPC leaders were against that), [7] support other market reform and thought liberalization in 1980s, especially devoting more time on passing the laws for protecting market orders when he was in the position of the Chairman of the Standing Committee of the National People’s Congress. Regretfully, Wan Li didn’t do his best to avoid the casualties in Tian’anmen Square protests of 1989 and the further thought liberalization after 1990s. After Wan’s visiting for foreign countries, on May27th, 1989, he made a statement showing his support on Deng Xiaoping’s decision on using force to suppress the student movement in Tian’anMen Square which was different form his former support on Zhao Ziyang, who sympathized on student movement. [8]

What we can learn from Wan Li and the agricultural reform?

What can the current CPC leaders should learn from Wan? Leadership can learn to be more courageous with market reform initiations for China. What we see is, in the last 30 years, free market reform gives more Chinese an opportunity to take their own responsibility on their own life, liberating their entrepreneurship to create more goods and ideas for exchanging and improving different people’s life. What we also see is, the remaining part of central planning system, such as the economic monopoly of state-enterprises, too many administrative examinations and approvals for opening private sectors or non-profit mutual help organizations are disrupting different individual Chinese to seek for their own dream and happiness, which also influences the stability of Chinese societies. As the new Chinese leaderships have admitted for many times, market reform should be continued and they are really doing this such as cancelling many administrative examinations and approvals for private business. [9] Besides, it’s also necessary to deregulate the non-profit mutual help group to let the self-governing function among different individual be smoother which could also help government to reduce the burden on governing. And for Chinese people, they should learn from the courage from the 18 farmers in Xiaogang Village and trust that they themselves can take care of themselves much better than government and gradually understand the benefit from market process by themselves.

–

Notes:

[1] Wan, Li (2009) How did the agricultural reform start? Beijing: Guangming Online. Available: http://www.gmw.cn/02sz/2009-02/01/content_919690.htm [Accessed: 25 August 2015]

[2] Yi, Jing (2008) The change of people and land in Xiaogang Village. Beijing: People’s Daily Online. Available: http://house.people.com.cn/GB/98384/99155/99181/8174533.html [Accessed: 25 August 2015]

[3] Deng, Xiaoping (1994) The Selected Works of Dang Xiaoping (Volume II). Beijing: People ‘s Publishing House, pp 315-317.

[4] Yao, Yilin (1980) Report on the Work of the Government (1980). Beijing: the Central People’s Government of the People’s Republic of China. Available: http://www.gov.cn/test/2006-02/16/content_200778.htm [Accessed: 25 August 2015]

[5] People’s Daily Online (2004) The household responsibility system opened the door for agricultural reform. Beijing: People’s Daily Online. Available: http://www.people.com.cn/GB/shizheng/8198/36907/36908/2732004.html [Accessed: 25 August 2015]

[6] Griffin, Keith (1987) The structural reform and economic development of Chinese rural area. Hong Kong: The Chinese University Press, pp.222-224.

[7] In 1980s, Chinese leadership was separated into two camps. One is for the innovationists leaded by Deng Xiaoping, and Hu Yaobang, Zhao Ziyang, Wan Li, and son on were the members of it who supported market reform and a certain degree of political reform such was the freedom of speech and more political election; another is for the conservatives leaded by Chen Yun, Li Xiannian and so on, who supported central planning economy with only a few factors related with economic regulation and strongly disagreed with political reform. After the stepping down of the former Chairman of the Central Committee of CPC, Hua Guofeng in 1981, Deng Xiaoping totally became the most powerful leader of China. But as Chen Yun and Li Xiannian also had a strong influence in the party, the market reform was disrupted by the conservatives many times. More information see: Zhao, Ziyang (2009) Prisoner of the State: The Secret Journal of Premier Zhao Ziyang. New York City: Simon & Schuste, pp.91-94.

[8] Zhao, Ziyang (2009) Prisoner of the State: The Secret Journal of Premier Zhao Ziyang. New York City: Simon & Schuste, pp.8-14.

[9] More in formation about Chinese market reform, see Zhang, Weiying (2015) The Logic of the Market: An Insider’s View of Chinese Economic Reform. Washington, DC: Cato Institute.

–

William Hongsong Wang is a researcher from the Shalom Institute and has graduated with a masters degree of Austrian Economics from the Universidad Rey Juan Carlos in Spain (King Juan Carlos University).

If you like this article, please scan the QR code below on Alipay for sponsoring the author:

Dr. Zhu Haijiu

On August 11st, China Central Bank, the People’s Bank of China (PBC) declared to downturn the central parity rate of Renminbi (RMB) against foreign currencies, then the exchange rate of RMB decreased 4.4% from August 11st to August 14th. World market was shocked by this devaluation. Chinese Austrian economist Dr. Zhu Haijiu was interviewed by Chinese media about why Renminbi is in devaluation.

The large devaluation of exchange rate shows the earlier devaluation of RMB in Chinese domestic market

The price of a country’s currency should be the same whether you use the domestic or foreign commodity to measure it or not. So the large devaluation of exchange rate of RMB shows the earlier devaluation of it in Chinese domestic markets.

Journalist: After PBC decided to adjust the central parity rate of RMB on August 11st, the exchange rate of RMB has dropped several points in a day. How do you see the drop of RMB’s exchange rate?

Zhu Haijiu: The drop of the exchange rate is the inevitable result from the former inflation, which also represents the Chinese economy is shifting into the period of crisis. On one hand, inflation advanced labour cost, which makes investment unprofitable; on another hand, the high asset price caused by inflation cannot maintain itself, which is on the ways of dropping. This prompts capital to outflow, which makes the drop of the valuation of domestic currency and makes the exchange rate depreciation become inevitable.

The price of a country’s currency should be the same whether you use the domestic or foreign commodity to measure it. But when Chinese people are touring in foreign countries, they can find that the price of many commodities in China is higher than the price of the same goods in foreign countries. And it is unreasonable to use the same amount of RMB for buying more goods in foreign countries. Market will let the two prices be at the same level. So the large devaluation of exchange rate of RMB shows the earlier devaluation of it in Chinese domestic market.

“Inflation” and “currency stabilization” cannot be got at the same time

It’s very easy to understand, the more goods an economy has, the more it will devalue, so as the same situation as in currency supply.

Journalist: The opinions as to why this devaluation of RMB happens is that China is facing both economic downturn and decline of foreign exchange reserve (for example, report from PBC today says in this July, funds outstanding for foreign exchange declined for ¥308 billion), but meanwhile the supply of basic currency will still keeping growing, which makes the devaluation of RMB inevitable. What do you think about this opinion?

Zhu Haijiu: According to economic theories, if the foreign exchange reserve declines, the supply of basic currency should also decline. But in the past year, on the contrary, the supply of basic currency was increasing, which meant that credit expansion didn’t stop but was growing stronger if we consider this offset the decline of basic currency caused by the decline of foreign exchange currency. During the past, I’m afraid that the overvaluation of RMB was kept artificially. So the sharp fall in the value of RMB is both the error correction for the overvaluation and the error correction for exchange maintained artificially.

“Inflation” and “currency stabilization” cannot coexist at the same time, so the devaluation of RMV is an unavoidable result from inflation. It’s very easy for understanding, the more goods it has, the more it will devalue, so as the same situation as in currency supply. The inflation has resulted in excess capacity in the real economy: productions cannot find buyers, the asset prices of real estate and stock raised and then dropped. Neither could currency avoid that situation. The drop of valuation of RMB happened just after the stock crash last month. The currencies of the countries that heavily rely on product factors exporting, such as Australia Dollar, Brazilian real and Russian ruble all have a large fall, so we can say RMB has held on firmly for a while.

For a period of time, PBC tried to maintain the price of assets by issuing more currency to avoid capital outflow. But this devaluation of RMB proves this way doesn’t work, which means we cannot avoid economic downturn by using currency. Sooner or later market rules will function which China Central Bank PBC has no choice but to follow. We can say this devaluation of RMB is “the winning of market but the failure of central bank ”. Economic crisis and the devaluation of currency are the inescapable results both from fiat money system and the currency manipulation from central bank.

Fiat money is unstable, which has the tendency of collapsing by itself. The increase of fiat money will surely accumulate debt, and debt should always be returned as obligation. When government tries to issue new fiat money to return the former debt, the devaluation of fiat money happens. If a government issues huge amounts of money, so the people in that country only need to use these money to buy foreign goods. You don’t need to work hard then you can live in a good life by those money. Will a good life suddenly fall into you lap? If it’s possible, the richest country on earth may be Zimbabwe. In the situation of inflation, the devaluation of currency must be discovered by market, which makes it impossible for government to cover and forcibly maintain the value of the domestic currency. In the 1990s, British government was beaten by George Soros is a good case for that.

Currency wars are bad for economy

The devaluation of currency artificially only increases the assurance of money and increases the price, not increasing the real wealth.

Journalist:Some people say, the devaluation of RMB this time is the currency war against the devaluation of currencies of other countries. What do you think? Is currency war a real matter?

Zhu Haijiu: As what has been said above, the devaluation of RMB was caused by market rules, not the currency way that should de faced. Any idea that wants to use currency wars to improve economic situation should be abandoned. Fight for currency wars will disturb the process of market, which is harmful for economy. What we need to worry about is not the devaluation of currency, but to not let it devaluate.

The named currency wars cannot increase the wealth of a country. The thought that if a country has more foreign currency, then it will be richer is an idea of the outdated mercantilism. The chief economist of Industrial Bank Co., Lu Zhengwei said after the devaluation of RMB, China’s economic growth can easily achieve 7.5%. It seems that economic situation will become better if the currency devaluates. This point of view is untenable. The devaluation of currency artificially only increases the issuance of money and increases the price, not the real wealth. Of course, if the devaluation is conforming the market rules, things will be different.

Currency exchange rage is just a rate of exchange, which cannot presents the change of wealth. If you buy more products in foreign countries, more currency will flow to these places, then the price increases; in the condition of free trade, this money will flow back to your goods, because your products have become cheaper. The creation of wealth doesn’t rely on central bank, but on the free movement of commodities, currency and personnel. Over issue of currency or manipulating money artificially all are harmful to the creation of wealth. So in this perspective, central bank is the crime culprit which disrupts economy. It is very hard to achieve the marketization of exchange rate if central bank exits. Of course, what PBC is doing this time is conforming to the marker process, which is advisable.

The change of currency rate is a signal of economy, like the temperature fluctuation of thermometer is the signal of temperature. The way you put the thermometer into water and reduce the temperature artificially in water cannot reduce and present the real atmospheric temperature. Likewise, manipulating currency artificially and starting currency wars will never improve economic situation and make the pricing signal become a failure and let economy get more troubles. The entire world should give up currency wars and make free market and free trade their goals.

Translated by William Hongsong Wang. This translation is cooperated with TBI Translation.

–

Dr. Zhu Haijiu is the professor of School of Economics of Zhejiang Gongshang University and the researcher from the Shalom Institute.

If you like this article, please scan the QR code below on Alipay for sponsoring the translator:

约会市场太乱,太不公平,需要政府管一管!

这将是一条漫漫之路,但愿有那一天,人们能把“社会”和“人民”视作自由而互利结社的个体组合,不论他们是谁,不论他们希望怎样结社,无论他们想在哪里生活与工作。

地球比你想象的大,价格的力量推动了创新、集约化和资源保护。资源并不是在自然中被发现,而是因着人的大脑被创造。

本文为澳大利亚悉尼麦考瑞浸信会(Macquarie Baptist Church)牧师马克·罗伯茨(Mark Roberts)的讲道。 繼續閱讀 “基督信仰是一种宗教吗?"

诚然基督耶稣可以坐拥万国。但,基督拒绝了。

你必須登入才能發表留言。