This article is the English version of the speech draft on the conference for Instituto Juan de Mariana on March, 25, 2017

William Hongsong Wang

1. Before the 1978 reform

Javier and Antonio illustrated both the liberal thoughts and the economic and reform situation of China. These parts are fascinating. China had not only liberal views in the epoch of 2000 years ago but also had other free market and free society oriented thoughts in the last 2000-year history. These thoughts, with the thoughts from Laozi and Confucius, like Javier has demonstrated, influenced Chinese economy. Before the trade ban in the early of Qing Dynasty, Chinese people were trading with the rest of the world for more than 2000 years. In the epoch of Emperor Kangxi, to control the whole country, Qing Dynasty started trade ban with foreigners. Meanwhile, the ideology control becomes more restrict than before. Literary Inquisition makes it almost impossible to produce new thoughts in social science. In 1776, Adam Smith published his famous The Wealth of Nations, who systematically studied economic science. Because of the trade ban and ideological control, China started falling behind the Western world.

The Opium War in 1840 broke the nature status of the old Chinese political and economic system. Qing Dynasty was beaten by the United Kingdom in the war and was forced to open some trade ports for international commerce.

For banking system, Chinese banking system was also not entirely monopolized by the state in the last 2000. George Selgin from Cato Institute studied the free banking system in the late 1800s in Fuzhou, Fujian Province of China, where people were using their currency without governmental currency intervention.

China ended its monarchy in 1912. After the Republican Revolution, China Republic of China was established. The period of the Republic of China was in War Time. For dealing with the wars, the Nationalists established China’s first modern central bank that started issuing fiat money in 1828. The establishment of China’s first modern central bank was also the research of my Ph.D. thesis. After the creation of china’s first central bank, China quickly suffered from hyperinflation. During the second Sino-Japanese War (1938 to 1945), the average inflation rate of China was 174%. In the period of the Communist Revolution, from October 1947 to the middle May 1949, the peak month and Rate of Inflation was 5,070% in April 1949.

Hyperinflation rate destroyed Chinese economy, and the Nationalist Government withdrew to Taiwan in 1949. In the same year, Communist Party of China established the People’s Republic of China, which started the separation between China and Taiwan.

As Antonio has demonstrated the period of Mao Zedong from 1949 to 1976, we will go deeply to explain the Chinese market reform, which started after the death of Mao. As Antonio has shown, the top political reformers, like Deng Xiaoping, played a critical role to eliminate governmental intervention in the economy and people’s daily life. But China’s market reform was started by ordinary citizens who wanted to use the free market to improve their life instead of the centrally-planned system. After people successfully restored the market, top politicians started to promote the rule of law.

2. The start of the reform, in the case of Xiaogang Village

Now let me tell everyone the story of Xiaogang Village.

Before and during the Cultural Revolution, all of the lands, agricultural tools and harvest belonged to the government. Farmers were not allowed to eat the agricultural productions on the farms they were cultivating. Many times as the local government had to do greasiness in Cultural Revolution, impractical agricultural plans were demanded that made it impossible for farmers to feel incentivized to do their work, provide goods, and earn money. If the local bureaucrats wanted to get promotion or praise from their seniors, it’s’ better for them to report massive political and economic movements to attract attention from their bosses even these plans were entirely infeasible. Many farmers died from starvation, and many were executed or punished for not obeying the bureaucrat’s orders by eating the harvest from their land.

In the spring of 1978, to resist drought and extreme poverty 18 farmers in Xiaogang Village of Anhui Province began disobeying central plans from senior officials by farming for their needs and the needs of the local free market to make a living. They separated the public farms amongst every individual. All of these people were responsible for their farms and crops and tried their best to grow agricultural products based on their market information. Of course, it was illegal at that time, but people there were so hungry that if they didn’t enact the reform themselves, they would not have survived.

This spontaneous, organic change was growing in many villages in the Anhui Province because farmers found that planning their “own" lands could help them earn more money and eat more food which was better than waiting for centrally-planned orders. The economic situation in these rural areas changed rapidly in just a few months after the new free market tests. That year, the farming team of Xiaogang Village’s total grain output was 66.5 thousands kilograms, which was equivalent to the sum of the total food production from 1966 to 1970; total production of oil (mainly groundnut) was 17.5 thousands kilograms, which was equal to the amount in whole past 20 years. Due to the development of output, a total income of the people in Xiaogang Village was over 47,000 Chinese Yuan, which was 400 Yuan per person and was 18 times higher than the previous year. Famers called this new agriculture institution as “household responsibility system” (包產到戶). This agricultural reform started the famous Chinese “Reform & Opening up" nowadays.

At this time, the change was becoming a hot political argument in the Communist Party of China (CPC) itself. Some local politicians allowed farmers to do market reform, but some did not because they didn’t want to take the risk of losing their jobs or being put in jail for enabling reform without the permission of China’s political leadership. After hesitating for a few months against widespread resistance to deregulation reform among top leaders in the Chinese government, Wan publicly supported the agricultural reforms occurring in the Anhui villages.

Used with the permission of the Central Committee of CPC, other parts of China’s rural areas gradually started doing the household responsibility reform, which allowed every family of farmers to be responsible for their profit or loss on agricultural production. The consequence of the reform was evident. The year-on –year growth rate of gross agricultural output of China was 8.6% in 1979. The grain production was 33.12 million tons, which was also 8.6% higher than in 1978. The total grain yield increase in 1978 and 1979 was 49 million tons, which never happened after the establishment of Communist Regime in 1949.

Seeing the obvious result of the agricultural reform, China’s top leaders, like Deng Xiaoping, who were taking a wait-and-see approach to the situation, finally decided to support the reform at the end of 1979. In 1980, Deng Xiaoping made a speech about that, “After we have introduced more flexible policies in rural areas, the result of the Household Response System was so obvious, which was changing the villages who had adopted the system. … The majority of the production teams in Fengyang County, Anhui Province who accepted the new system has totally changed their economic situation.”

At the same time, it was quickly promoted to other provinces over the next few years and resulted in rapidly expanding agricultural production. In 1982, a growth rate of the gross agricultural output was 33.4% higher than in 1978; the rate of increase of oil crops was 126.5% greater than in 1978; the growth rate of per capita income of Chinese farmers was 102.2% higher than in 1978. In 1982, the market reform in agricultural industry was finally made legal through the approval of Chinese Central Government and was officially named termed the Household Responsibility System.

Not only farmers were supporting themselves through market reform, but also the people from the major cities and towns. Many central planned local factories started to be managed by the local population themselves, which are called Township and Village Enterprises (乡镇企业). People near sea also began smuggling for surviving in the early 1980s. Besides, Special Economic Zones, which in some degrees copied the economic model of Hong Kong were also being adopted.

Doing business inside China and doing trade with foreigners were quickly legalized in the middle of 1980s. If the top Chinese politicians did not support the spontaneous reform, it would be impossible to legalize the spontaneous free market institutions. During the 1980s, Deng Xiaoping was the core of the reformers. Prime Minster Zhao Ziyang was reasonable for the economic reform part. General Secretary Hu Yaobang was reasonable for the mind emancipation movement. People were allowed to talk about politics again. Intellectuals were openly debating on which kind of political and economic system should China adopted. Their thoughts were even posted on the Party’s newspapers. In the leadership of General Secretary Hu, the Party was even trying to separate the management of the Party and the Government. Many famous free market-oriented economists, like Mao Yushi and Zhang Weiying, also participated the debate and the reform of economic institutions. The atmosphere of the liberty of free speech was obviously much better than the current China.

3. Crisis in China, in the Case of Real Estate Industry

As Antonio has demonstrated, the Tiananmen incident in 1989 ceased the political reform. Though in the urge of Deng in 1992, China restarted to reform the economic issues, but the majority of economic policies were Keynesian Economics-oriented, as Antonio has presented. The State Owned Enterprises owned by the Central Government were cut into only 138 in the April of 2016. But the majority of them controlled the majority industries of a military, telecommunications, oil, insurance, banking, tobacco, rail passenger and freight, postal, port, airport, radio, television, publishing, etc. Some local governments were even managing restaurants. Though the State Owned Enterprises were supported by the state, many of them are losing at least millions of money every year. As many of them are borrowing the money from Commercial banks, and because of the fiat money created by central banking system the bankruptcy of State Owned Enterprises will cause a systematic economic crisis in China.

One of the most suffered industries was the real estate industry. Antonio and I also made an empirical research on Chinese real estate industry based Austrian Business Cycle Theory. This study will be published on Proceso de Mercado this June.

According to Austrian Business Cycle Theory, the new credit created by central banking would decrease the interest rate and prolong the industries, which would not be seen in production structures by the nature interest rate. Later as these newly created industries are credit oriented, consumers would possibly not buy these products. Then interest rate will raise, bankruptcy would happen in industries. As time is very limited, we are not going to demonstrate the details of Austrian Business Cycle Theory.

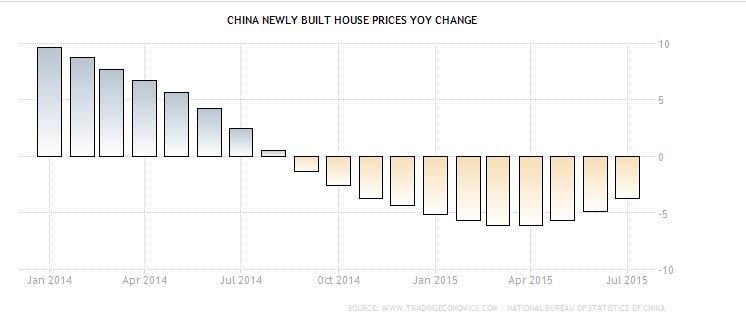

From September 2005 to January 2009 was the first cycle. In the first reporting period, the growth rate of salary is almost in the same trend, which means people still could buy the houses. But as we know, once central bank uses monetary stimulus to accelerate real estate industry, the gap between the growth of average wages and growth of average real estate price would become bigger and bigger. The duration of this cycle was three years and five months.

The length of the second period was three years and two months. Now we find that in this sub-economic cycle, after the decreasing of the year to year housing price happened in 2010, PBCO immediately issued more credit in both the developers and consumers part of CREI in 2011. It seems that the monetary stimulus plan was useful, but we should understand the economic process is not a static process, but a dynamic one, which consists of different productive stages. As the artificially low-interest rate appears in CREI, investment goes into there instead of other industry, which causes discoordination and destroys productivity in the full productive stages. Besides, in those productive stages, because the value is subjective, dynamic and implied, it was impossible for governments and central banks to know what people want to produce and consume, and any governmental intervention would cause chaos in society, so as the same as the investment in CREI.

The malinvestment posed by the fractional central banking credit did have its effect during this sub-economic period. According to news reports, China already had at least 40 ghost cities where had built houses, hotels, schools, roads and other public facilities but almost nobody lives there.

From February 2012 to January 2015 was the third business cycle in real estate industry. According to news report, there are 12 empty cities appeared in 2013 because of the former economic stimulus plan

From January till now are the fourth business cycle. According to the news report, there are at least 50 ghost cities in China in 2015 constructed by new real estate in recent five years, where the population of each city is less than 5,500 / sqr km. The top 10 ghost cities which have the population less than 3,900/ sqr km.

Besides that, there are at least three real estate enterprises bankrupted since 2015. They owned more than 880 millions debt.

4. Suggestions

As China has a lot of problems, we have to reform China. Here are some tips in the Austrian perspectives.

Concepts lead to actions. And actions lead to change. First, China should focus on the education of free market and property rights. We have to realize that even though China has achieved a very great market reform driven by market rules, the country has a long tradition of absolutism, which makes the people nowadays still believe that China needs one party political system and central planning.

Besides, in China, if you want to do business, especially big business, you have to have connections in the government. There is a particular word to describe this Chinese character crony capitalism, Guanxi. If Chinese people do not understand the rule of law and the principles of economics, they will continue using guanxi for their benefit.

Second, we propose the privatization of SOEs, which is the primary concern of China’s economy. We conclude from our study that the inefficiency of SOEs reduces the credit to private enterprises and provoked problems to commercial banks. SOEs are also invading property rights, which should be eliminated entirely.

Thirdly, China needs to abandon the capital controls and the fixed exchange rate policy and welcome free banking. The free flowing of money and the liberalized interest rates would increase the competition in Chinese industries. Of course, finally China has to adopt free banking to avoid the systematic economic recession and cycle caused by central banking, but the current proposal is more practicable and would make it easy to take free banking in future.

Fifthly, China has to build an independent judicial system. An independent legal system could avoid the collision, or guanxi, between the officials and entrepreneurs, and provide a fair judgment for ordinary citizens.

Finally, China should decentralize the political power. The diversity of culture and custom makes impossible to keep a central planning system in a more and more pro-market Chinese society in the future, which means a decentralized and a federal democratic system is becoming more and more necessary.

你必須登入才能發表留言。