Antonio Vegas García

Recently, we have been exposed to a barrage of news from China: the rising worries about its economic growth, the recent plunge in the Chinese stockmarkets, the devaluation of the yuan, the announced drops in interest rates, as well as in the cash reserve bank ratios, the Purchasing Managers’ Index (PMI) fell, etc. [1]

Nevertheless, the bad news is not the economic indicators, but the government’s reckless interventions in these days. The government seems risking the initiated path by the Economic Reform towards the development, a movement in the bad direction that could become the next Great Leap Backward in the Chinese economic history.

In order to make it clear, we should build up a general idea about the Chinese economy to be able to put together all the pieces of the Chinese puzzle. The chinese economy is huge and extremely diverse (even we can name it as a dual economy in Lewis terms) but we can state that the Chinese prosperity looks like more a mirage than a reality. Of course that double-digit growth has permitted that China has lifted 600 million people out of poverty during 1981-2004 [2], but at the same time, it has sown the seeds of the future economic problems, the shadow of the Chinese prosperity.

Which are those flaws? Mainly the heavy-handed and commanded economy, through the financing part of the economy, whereby the government extract wealth from the people (mainly controlling the interest rates and the exchange rate of the currency), that is used afterwards to prop up the banks that have chunks of bad loans, thereby allowing them to carry on lending money to the unprofitable SOE (State Owned Enterprises). In short, the government has built a system in order to control every single aspect of the economy, which is generating long-term problems, such as shadow banking (even though the term includes a myriad of different non-conventional institutions).

This financial repression can be illustrated with the example of drug prohibition. When the government attempt to forbid the drugs what it gets is a black market where the people can sell and buy drugs according to human necessities (that are subjective), but the black market is not regulated and it is not safe enough for the users, thereby damaging the health of the participants. The more important (and the more repressive is the prohibition) is the forbidden necessity for humans, the more serious will be the suffering of the population. In the case of China’s financial repression it’s exactly the same: given that chinese people neither can take credit freely nor save their money, a black market pops up to satisfy the necessities, with credit of bad quality, thereby jeopardising the long-term perspective of chinese economy.

Under this outlook, the recent headline-grabbing news about china are not surprising whatsoever, but they are showing that the government is doing whatever it takes in order to shore up the binge. That government disposition is a helpful information, since in China everything is depending on the government. Until when the binge will last? Until the government desire unless it runs out of money, like once Larry White told me very cleverly. After all, it looks like that the government does not want to stop it.

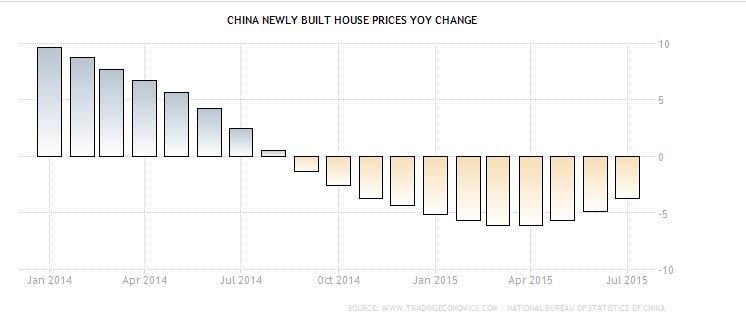

With a slumping housing market, with an entire year of steadily lowering housing prices (see figure 1), the Central Bank of China has been lowering the interest rates one after another (see figure 3), jointly with the cash reserve ratio.(see figure 2), in a last attempt to foster the Chinese economy up to the promised 7% growth rate.

Figure 1: China newly built house prices YoY (Year on Year) change (%) Jan 2014-Jul 2015

Source: Tradingeconomics.com

Figure 2: China cash reserve ratio big banks (%) 2011-2015

Source: Tradingeconomics.com

Figure 3: China interest rate (%) 2012-2015

Source: Tradingeconomics.com

I remember that the summer of 2013 was when I really opened my eyes about the Chinese economy, it was the Shibor (Shanghai Interbank Offered Rate) shock. After an increase of the lending in the first 13 days of June never seen before in history, the interest rates in the interbank market soared to a 12% rate for the seven-day repo [3]. The central bank forced the big banks to lend money to the small banks (with the argument that the overall liquidity within the system was enough), thereby rejecting the inquiry of the financial institutions of injecting more liquidity. One month later, the central bank had to inject a massive amount of liquidity in the system, at the time that the interest rates were lowered as well as the cash reserve ratio. The yield curve (an indicator that it’s used to foresee financial problems in an economy) has not stopped flattening ever since.

The recent plunge in chinese stockmarkets is anecdotal. From the early 2014, the stock indexes reached a high level without any reasonable explanation and mainly driven by credit financing (9% of market capitalization according to Credit Suisse). The price earnings ratio or PER (that is calculated dividing the price of a share over the ratio between the earning of the whole company over the number of shares, namely, the earnings per share, EPS), was in median terms 64 in Shenzhen stock exchange, whereas it is considered that a PER higher than 25 is expensive [4]. The Shenzhen case was paradigmatic. A clear indicator that the Shenzhen Stock Exchange was flying too high.

Therefore, the recent drops in those indexes have been obvious and they have been noticed in advance by Bloomberg or The Economist. And the drops will likely continue for a time. Even though, they are not so troublesome for the Chinese economy in the short-term (because the stock market is not so developed in China as in western countries; its relative size to the economy is small, 40% of the GDP whereas in USA is more than 100% of GDP and the financial culture in chine is still limited) but they will be crucial in the long-run. What is true is that it shows more than ever the shadow of the Chinese prosperity, the financial flaws of the Chinese economy. And the recent actions of the Chinese government are the most burdensome. Let’s see why.

Firstly, in China is urgently needed a complete financial liberalisation, where the bank interest rates can be fixed by the market, with more share of private banks in the economy and the banks being able to give lending according to market criteria and not with political criteria. This will bring the second opening of Chinese economy (the financial opening) and will push the world to a new level of financial globalization. Moreover, it would foster the SOEs to a new level of competitiveness, would give more resources to Chinese private companies and would reduce the power of the government. In other words, it would bring more freedom to Chinese people at a time the shadow of Chinese prosperity shrinks. However, as the recent actions of Chinese government tends to broaden the influence of public sector over stockmarket, the financial liberalisation has fallen to bits.

Chinese stockmarkets were always seen as not so trustworthy but nowadays more so than ever. The government introduced a curb in selling Chinese equities and also it undertook and equities purchasing programme, spending public money in order to prop up the stockmarket bubble. That is added to the enormous requirements that the companies have to fulfil, the daily limitation that a share cannot raise or drop more than a 10%. That is undermining the last bit of truth on Chinese equities.

Secondly, as the equity financing is necessary for Chinese economy in order for the companies to be able to diversify their financing portfolio (debt and equity). Investors were always wary about the Chinese economy and at the time they were surprised that the Chinese economy was resilient to every kind of damage or bad indicators. Investors finally concluded that in China, everything is about its government.

Overall, it looks like that, even though China has advanced until now quite rapidly, a recession would be a necessary step towards China’s development, since the goverment is reluctant to reduce its grip in Chinese economy and it will do whatever it takes to prop up its power, influence and command in Chinese economy. It’s a necessary step that the government runs out of money and the crisis in that sense could be an opportunity. The last government interventions illustrate the government’s disposal to maintain the statu quo, even if that requires to risk the trust of international investors in China or risk positive results of the economic reforms.

Obviously, Chinese economy also has advantages, and it is reducing the importing of inputs to produce the goods that China exports, showing that China is improving in capital accumulation and the economy is more capable to design new products rather than buy them abroad. The attention is in the government’s side. The government still have weapons to shore up the financial mess and its influence on the market, but the money and the time are running out nowadays. What will be the next episode? The crisis in China, will force the government to another set of economic reforms.

–

Notes:

[1] Bloomberg (2015) China’s Official Factory Gauge Shrinks Available:http://www.bloomberg.com/news/videos/2015-09-01/china-s-official-factory-gauge-shrinks [Accessed: 31 August 2015]

[2] CNTV (2014) China has lifted 600 million people out of poverty Available:http://english.cntv.cn/2014/10/18/VIDE1413584528072923.shtml [Accessed: 31 August 2015]

[3] The Economist (2015) Flying too high Available: http://www.economist.com/news/finance-and-economics/21579862-chinas-central-bank-allows-cash-crunch-worsen-shibor-shock [Accessed: 31 August 2015]

[4] The Economist (2013) The Shibor shock Available:http://www.economist.com/news/leaders/21652326-long-term-consequences-chinas-coming-stockmarket-correction-are-ones-fear-flying [Accessed: 31 August 2015]

–

Antonio Vegas García is a researcher from the Shalom Institute and has graduated with a masters degree of finance from the Universidad Carlos III de Madrid (Carlos III University of Madrid).